The markets continue to play down the speech of Federal Reserve Chairman Jerome Powell before the U.S. Congress. The stock market is in the red, bonds are selling off, and the dollar has strengthened across the currency market.

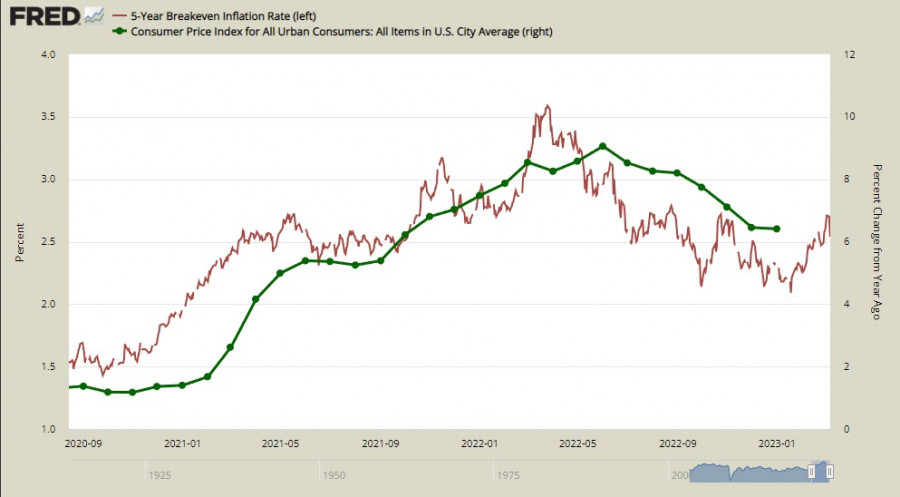

The Fed is clearly dependent on incoming data, so the coming reports will be important. The Nonfarm will be released on Friday, next week the consumer inflation report for February. There is a high probability that inflation will show an uptick after months of slowing, at any rate, the yield on 5-year inflation-protected Tips bonds has been rising since January, meaning businesses believe the current pace of Fed rate hikes is insufficient to return inflation to the target.

The futures market shows an 80 percent probability of a 50p rate hike on March 22, compared with 20 percent before yesterday. This is a tangible reorientation, and the dollar will strengthen for some time only on the wave of changing forecasts, even without any additional support.

Today, the focus is on the ADP report on employment in the private sector and the JOLTS report on open vacancies, increased attention is paid to the labor market, since wage growth and labor demand remain too high, which fuels consumer demand and, accordingly, inflation. Also pay attention to the Beige Book, data from Japan on GDP for the 4th quarter, and a little later – on inflation in China for February.

The week turned out to be busy, so the risk of high volatility will be present until Saturday, when the week of silence begins before the next Fed meeting.

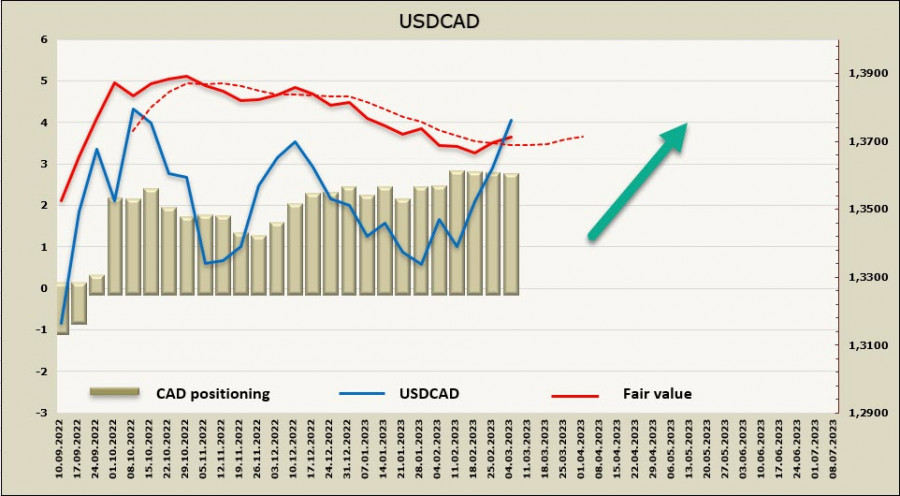

USDCAD

Today, the Bank of Canada will hold a regular meeting on monetary policy. No changes are expected, only an accompanying statement will be published, without new forecasts and a press conference.

The Bank of Canada has made it clear that it is taking a break to observe how effective the accumulated policy changes are. Taking into account yesterday's hawkish statement by J. Powell and the change in forecasts for the Fed rate in favor of a higher level, such a BoC position leaves no chance for loonie bulls, the yield spread will increase in favor of the dollar, which will have a decisive impact on the UASCAD rate in favor of its further increase.

Such a scenario is most likely, unless, of course, the Bank of Canada surprises the markets today and goes into surveillance mode, but still raises the rate by a quarter point. In this case, the USDCAD may roll back down a bit.

The estimated price in the absence of fresh CFTC data is turning up, which indicates short-term market expectations.

A week earlier, we saw a target at 1.3704, this goal has been worked out, and now we need to focus on the peak from October last year of 1.3976.

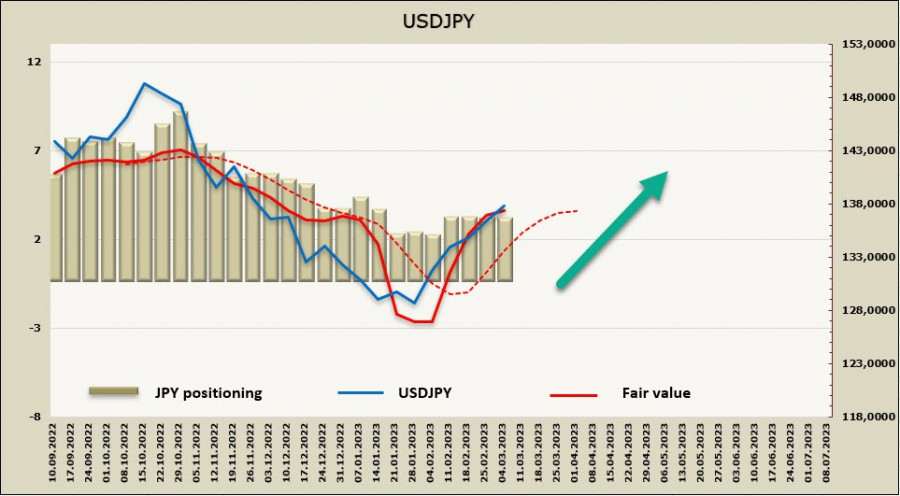

USD JPY

The decisive factor for the USD/JPY pair is not whether the Bank of Japan will tighten monetary policy, but when it will happen. On Friday, the last BoJ meeting will be held under the chairmanship of Kuroda, the markets are not waiting for changes, but it may well turn out that Kuroda will take the hit by announcing the necessary but unpopular changes, which will somewhat untie the hands of Kazuo Ueda, who is coming to replace him.

Japan's economy is sensitive to global factors, and the country has never avoided a recession whenever the US has entered a recession since 1990. Inflation has finally come to Japan (in January +4.3% YoY), for the Japanese economy, inflation is generally imported, that is, it can be assumed that if inflation goes up again in the US, it will go up in Japan, which forces tightening monetary policy.

What can be done? Markets estimate a 10p rate hike by the summer and another 10p rate hike by the end of the year. Sales of long Japanese bonds reached an all-time high in absolute terms in January, which suggests that markets are almost convinced that the Bank of Japan will change or exit the YCC in the short term. Changes in the YCC can occur in two ways; 1) extending the YCC range, for example, to +/-100 bp (currently +/-50 bp), 2) reducing the target maturity of the YCC policy, for example, to 2 or 5 years, from 10 years. A complete rejection of YCC will mean that the yield on 10-year bonds will jump to about 1.5% in accordance with the standard Fischer equation, where inflation plus the real interest rate equals the nominal interest rate. Taking into account the huge accumulated domestic debt, its servicing will rise tenfold, which will very quickly increase the budget deficit to record levels and bring down the Japanese economy into depression.

Therefore, attention to the results of the Bank of Japan meeting on Friday is increased, and according to its results, strong volatility is possible if Kuroda still announces a decision that is not expected by the markets yet, but is recognized as necessary.

The estimated price is much higher than the long-term average, it is directed upwards, there are no grounds for a USDJPY reversal to the downside.

The USDJPY has settled above the technical level of 136.70, the nearest resistance is 138.20, further 139.60. I expect the pair to rise further, unless the Bank of Japan decides to give us a big surprise on Friday.

The material has been provided by InstaForex Company - www.instaforex.comfrom Forex analysis review https://ift.tt/FMlQjce

via IFTTT