The absence of significant macroeconomic news and the silence of the Fed due to a quiet week before last week's meeting led to another calm day with low volatility.

The market leader remains the Australian dollar, which rose after the unexpected decision by the Reserve Bank of Australia (RBA) to raise interest rates. Trading in other currencies remains within a narrow range without prospects for strong movements. Risk appetite is decreasing after China showed a noticeable deterioration in its trade balance this morning, with exports declining by 7.5% YoY in May, which is significantly worse than expected and may indicate a slowdown in global demand.

Oil, after an optimistic opening on Monday due to OPEC+'s readiness to cut production to support price levels, has fallen, which may also indicate expectations of a demand slowdown.

The markets may be shaken by the European Central Bank (ECB). Several officials were scheduled to speak on Wednesday before the upcoming quiet week. However, in general, it should be expected that until next week when the results of the Fed meeting are known, market activity will be low, and trading will mainly take place within narrow ranges.

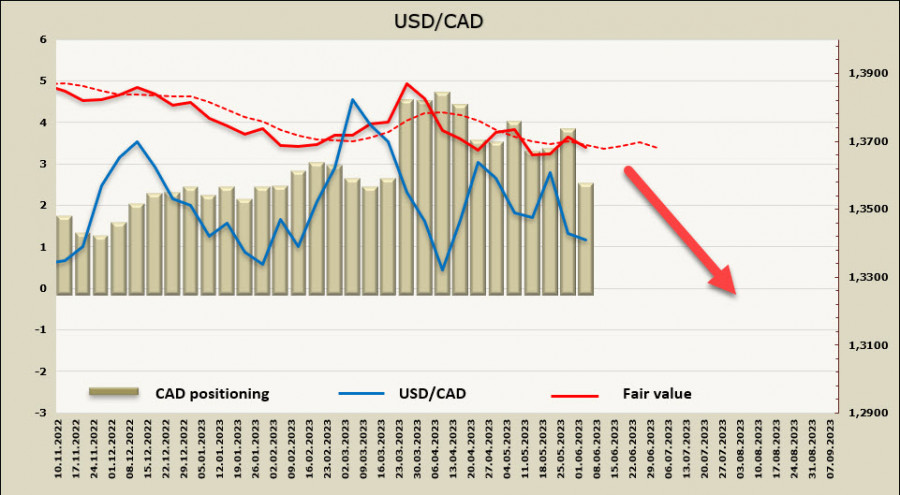

USD/CAD

The Bank of Canada was set to announce its decision on interest rates on Wednesday, which will be presented only in the form of a statement without any forecasts or press conferences. Expectations are uncertain; Bloomberg believes that the rate will remain unchanged at 4.50%, while some banks, including Scotiabank, believe that a quarter-point increase will still take place.

The Bank of Canada is currently exercising caution, and the key takeaway from the previous meeting is that the BoC will monitor the markets to understand if the restrictive policy is sufficient to return inflation to the target level of 2% and will be prepared to raise it if deemed necessary.

Inflation is likely to decrease in the middle of the year due to base effects, but at the same time, as indicated in the Bank of Canada's previous press release, a decline in labor market activity needs to be observed, which is not yet evident.

There are arguments for any decision. The 3.1% GDP growth in the first quarter exceeded the forecast of 2.3%, indicating that the Canadian economy continues to develop under conditions of excess demand, thus posing a high threat of inflation. The housing market is recovering faster than expected, and in April, the head of the Bank of Canada (BoC) stated that he expects housing prices to rise in the second half of the year, but recent data show that this process has already begun.

CAD has demonstrated the most significant improvement in sentiment over the past week. Speculative net short positions on the Canadian dollar decreased by $1.394 billion, totaling $2.2 billion, or just under 300,000 net contracts. This is the smallest bearish stance on CAD since early March.

The calculated price has turned downward, but the reversal looks unconvincing at the moment.

A week earlier, we anticipated that USD/CAD would continue to rise, which had quite obvious prerequisites. However, as of Wednesday morning, the situation has changed significantly. If the forecasts regarding a more hawkish stance from the Bank of Canada prove to be true, the probability of breaking out of the range to the downside will increase. We expect attempts to test the lower boundary of the technical figure at 1.3330, followed by support at 1.3295/3305. There are currently no strong reasons for significant movements unless, of course, the Bank of Canada surprises.

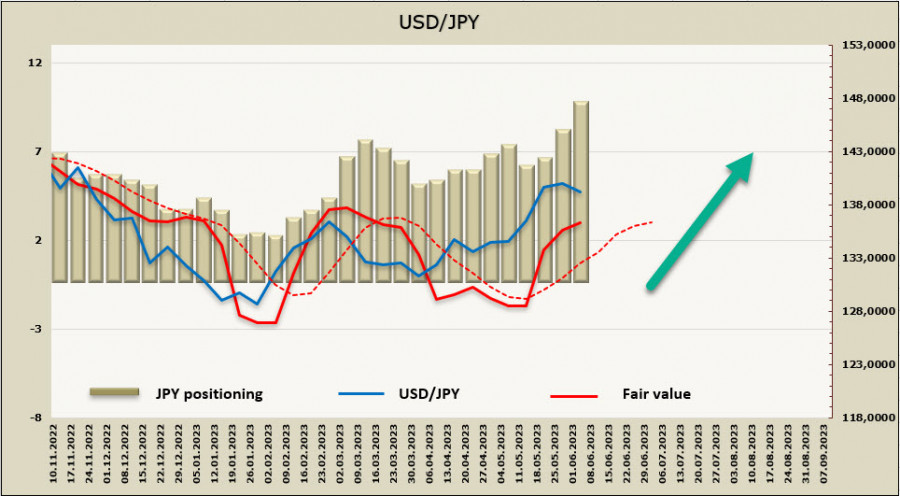

USD/JPY

Wage growth in Japan in April was lower than forecast, increasing by 1% compared to the revised 1.3% growth in March. A growth rate of 1.8% was expected. The market expected more significant growth based on the results of recent annual wage negotiations, but the data is not final yet, and it is likely that wage growth will be reflected in the May report. Nevertheless, there are no additional reasons for the Bank of Japan to show activity, and the upcoming meeting next Friday is unlikely to bring any surprises.

The weakening of the yen is justified, but it is unlikely to be considered long-term. Preliminary estimates of quarterly GDP show that Japan has emerged from a technical recession, and the Nikkei 225 stock index is breaking records. Activity in the manufacturing sector, unlike in the US, UK, and Eurozone, remains high, export volumes are growing, and the demand for the yen should objectively also increase, especially if commodity prices remain at current levels or decline.

Net short positions on JPY increased by $1.327 billion over the reporting week, reaching -$8.602 billion. The positioning for the yen remains confidently bearish. Investors have affirmed that expectations regarding a correction in the Bank of Japan's position towards tightening will not materialize. The calculated price is above the long-term average and is directed upward.

USD/JPY is gathering strength for a retest of the upper boundary of the channel, but since there is no clear driver, trading within the range or even a pullback to the middle of the channel at 137.60/90 is possible. In the long term, the trend is bullish, so after consolidation, an attempt to reach the local high at 140.91 with a target at the technical level of 142.50 appears more likely.

The material has been provided by InstaForex Company - www.instaforex.comfrom Forex analysis review https://ift.tt/AGkl0cQ

via IFTTT