The Caixin Services PMI index highlighted persistent challenges in China's economy, despite some stable activity in the manufacturing and construction sectors. The Chinese Caixin Services PMI dropped to 51.8 in August from 54.1 in July, compared to forecasts of 53.5, marking the lowest reading since December. It is needless to say that China's slowdown will inevitably exert pressure on the currencies of its major trading partners. Therefore, there's a higher chance that the New Zealand dollar (kiwi) and the Australian dollar (aussie) may fall further.

Saudi Arabia extended its 1 million barrel per day voluntary oil production cut until the end of the year, while Russia has cut 300,000 bpd. As a result, oil prices spiked, with Brent briefly trading above $90 per barrel. However, the increase in oil prices, while significant, was not as strong as one might expect, indirectly indicating a decrease in demand.

US Treasury yields have risen, and comments from Federal Reserve officials have been mixed. Waller stated that "there's nothing that is saying we need to do anything imminent anytime soon, so we can just sit there, wait for the data,". However, Mester from the Cleveland Federal Reserve Bank said the opposite: "From what I see so far, that we might have to go a bit higher,".

On Wednesday, the main focus was on the ISM report for the services sector. It is expected that activity in August will remain roughly the same as in June. If the forecast comes true, the US dollar will receive additional support. In general, the dollar is still leading gains even without this support.

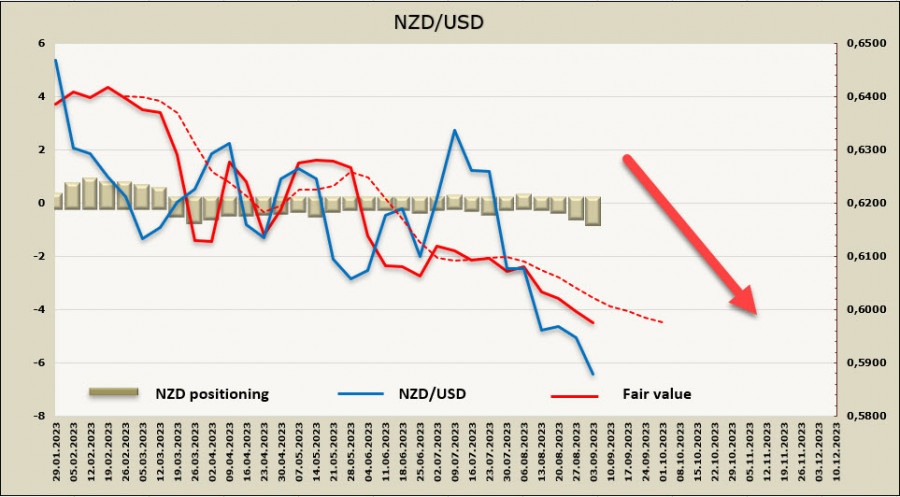

NZD/USD

New Zealand continues to see falls in export prices for New Zealand's agricultural products, which will lead to a significant decline in income across the industry. If the exchange rate weakens further, this could provide significant compensation, but it isn't possible to get something for nothing: it will lead to higher import prices, thus accelerating the move towards a recession. In general, the kiwi's depreciation aligns more with the government's plans than its strengthening, which supports the case for the kiwi's weakness.

Forecasts for the Reserve Bank of New Zealand do not anticipate a rate hike in the near term. The current inflation dynamics align with the RBNZ's projections, so it would be wise to watch and see how things go.

The economic situation can't be described as bad; business confidence has risen another nine points in August, although it's still in negative territory at -4, ANZ said. The latest figure is still the highest level since mid-2021. Expected own activity also jumped 10 points, to +11, and all activity indicators have increased, indicating a decline in recession prospects.

The net short position on the NZD increased by 0.2 billion to -0.62 billion over the reporting week, which means that positioning went from neutral to bearish. The price is below the long-term average and is firmly falling.

The kiwi has reached the lower band of the range, and from a technical perspective, there's a higher chance of a corrective rise to the middle of the channel at 0.604060. However, the fundamental picture suggests a breakout from the channel to the downside. If the kiwi falls from the channel, there are no significant resistance levels up to the October 2020 low of 0.5506. Therefore, the depth of the decline will depend on whether there will be any changes in the RBNZ interest rate forecasts.

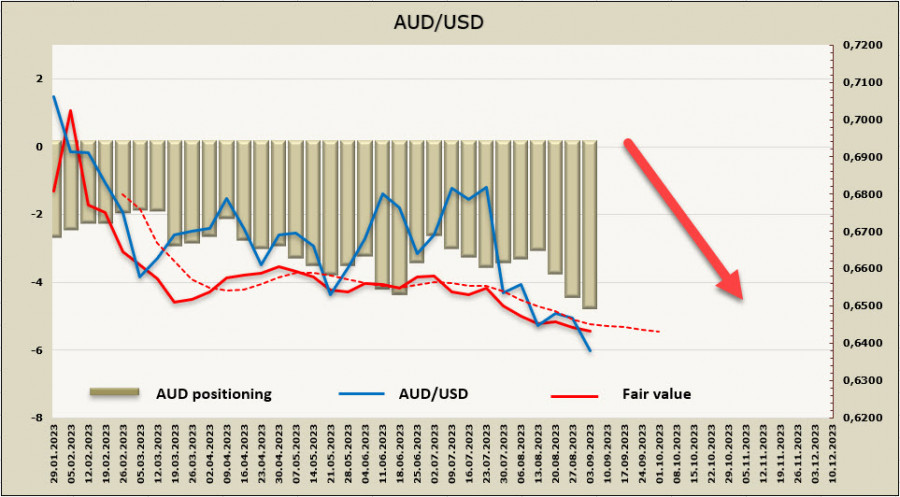

AUD/USD

The Reserve Bank held its cash rate at 4.1% for a third straight meeting because nothing significant has happened over the past period that would cause the bank to deviate from its "watch and see" strategy. The Reserve Bank of Australia considers the current rate sufficiently restrictive to return inflation to the target level within an acceptable time frame, namely to 3% by mid-2025. Since the RBA has almost two more years to achieve this goal, it is not in a rush; the main thing now is to ensure that inflation has indeed started to decline.

If it turns out that the measures taken are insufficient, the RBA may resume raising interest rates, but there's a low likelihood of such a move in the near future.

The economy is slowly cooling down, with the composite PMI falling to 47.1 from 48.2 in July, but it still remains in contraction territory. The TD Securities inflation index, calculated by the University of Melbourne, increased from 5.4% YoY to 6.1% in August, indicating that consumer prices grew instead of slowing down. GDP in the second quarter was 2.1% YoY, compared to 2.3% in the previous quarter, which was better than the forecast of 1.7%. Australia's trade balance data was set to be released on Wednesday, and RBA Governor Lowe is scheduled to speak, so we can expect increased volatility.

The net short position on the AUD increased by 0.4 billion to -4.5 billion over the reporting week, positioning is firmly bearish, and the price is below the long-term average leaning towards a succeeding decline.

The aussie has reached support at 0.6365, as we expected a week earlier, but it hasn't been able to firmly break below it yet. There's a good chance that the aussie will fall further, with the nearest target being the channel boundary at 0.6310/20. Beyond that, it is possible for the price to fall from the channel, with it moving towards the long-term low of 0.6172.

The material has been provided by InstaForex Company - www.instaforex.comfrom Forex analysis review https://ift.tt/Ut73lwk

via IFTTT