The latest US data turned out to be much weaker than expected. The Conference Board's Consumer Confidence Index fell for the first time in four months to 106.7 (expected 115) from a revised value of 110.9 in January. Durable goods orders fell more than 6% in January, and business investments also seem to be at a low level. Expectations for the recovery of the US industrial sector are not being met; now everyone is focused on the ISM report on Thursday.

As expected, the Reserve Bank of New Zealand left the parameters of monetary policy unchanged, and the tone of the accompanying statement was dovish, suggesting that the current interest rate level is sufficiently restrictive. Markets were expecting a more hawkish statement, so the kiwi immediately fell on the wave of disappointment after the results of the meeting were published.

Oil is trading near year highs, with Brent momentarily rising above $83 per barrel. Oil prices reflect several factors – rumors of OPEC+ readiness to extend production limits, the general recovery of the global economy and the associated risk demand, as well as a slowdown in the dollar's strength.

The data has virtually no impact on the market; yields changed insignificantly, and the US dollar fluctuated in a narrow range.

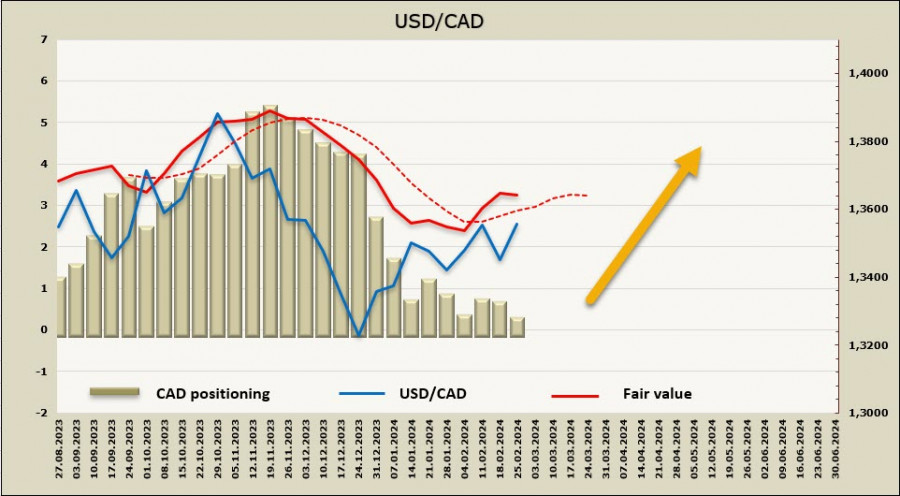

USD/CAD

Canada will release the GDP data on Thursday. After a disappointing 3rd quarter (-1.1%), market players expect a 0.8% growth, driven by increased working hours, a confident rise in exports, and stronger-than-expected retail sales data in December.

There are virtually no fundamental reasons to expect the CAD's growth. The dynamics of bond yields in the US and Canada are clearly not in favor of the latter, and the situation could change with a more hawkish position from the Bank of Canada, with the next meeting scheduled for next week. However, there is little reason to expect positivity here as well, as inflation in January decreased significantly more than forecasted, and therefore, the Bank of Canada is losing the last reasons to maintain a hawkish tone.

Most likely, the interest rate will remain unchanged at 5%, and routine statements about "waiting for new data to ensure a sustainable slowdown in inflation" will be made, but that's about it. The market's reaction is unlikely to favor the CAD, so it is possible that in the coming days, the loonie will continue to be under pressure, even though the US dollar is also losing its growth stimulus.

Overall risk appetite and rising oil prices are supporting the CAD, but to a lesser extent, as the Canadian economy is heavily dependent on the US. The higher the demand in the US, the higher the export and overall enthusiasm. Therefore, the key moment is the dynamics of yields, and it is currently not in favor of the CAD, which practically rules out the possibility of a turnaround in USD/CAD to the downside.

The short CAD position has been liquidated, with a weekly change of +340 million, and the overall bearish imbalance has fallen to -64 million. The bias is neutral; however, the price suggests further dollar growth.

USD/CAD is one step away from the nearest resistance at 1.3586, with the next target being 1.3620. If it manages to settle above this level, there are no significant resistances up to 1.3750/70, and only a change in forecasts for the interest rates of the Federal Reserve or the Bank of Canada could halt the rise.

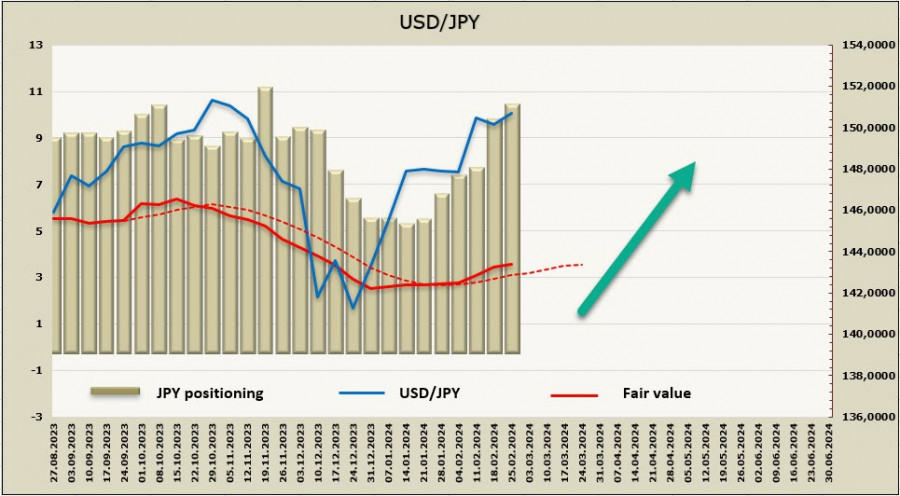

USD/JPY

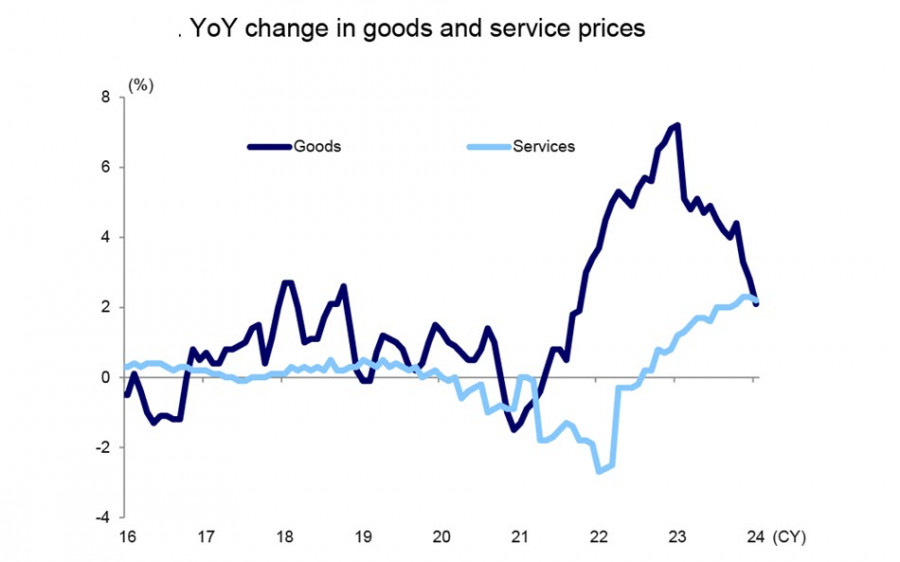

The core CPI fell to 3.5% y/y from 3.7% in December, and overall inflation slowed to 2%. The inflation of the core CPI is currently at its lowest level since March 2022 and exactly matches the price target of the Bank of Japan.

Compared to the 2.8% growth in December, goods prices rose by 2.1%, representing a significant slowdown. Services showed +2.2%, and for the first time in a long period, the growth in prices in the services sector exceeded the growth in prices for goods.

Mizuho Bank predicts core inflation will slow to 2% as early as summer.

Japan's economy remains in a growth phase, but the recovery momentum is weak. The question of whether the BOJ will raise the short-term interest rate to zero in April is considered resolved, and the situation will not change despite two consecutive quarters of real GDP contraction and three consecutive quarters of declining consumer and capital spending, which essentially determine the sustainability of domestic demand.

Additional rate hikes are not expected, as core inflation is slowing quite rapidly, and the yen will begin to strengthen when the European Central Bank and the Fed start lowering rates.

The net short JPY position increased by 819 million to -10.064 billion during the reporting week. The yen is just a step away from the November record low, which suggests that the yen will weaken further. The price is rising.

For two weeks, the yen has been trading in a fairly narrow sideways range just below the multi-year high of 151.92. We assume that trading will continue with low volatility, with slow growth towards 151.92. There is no basis for a downward retracement, given the growing risk appetite and the BOJ's ambiguous position.

The material has been provided by InstaForex Company - www.instaforex.comfrom Forex analysis review https://ift.tt/KIherb1

via IFTTT