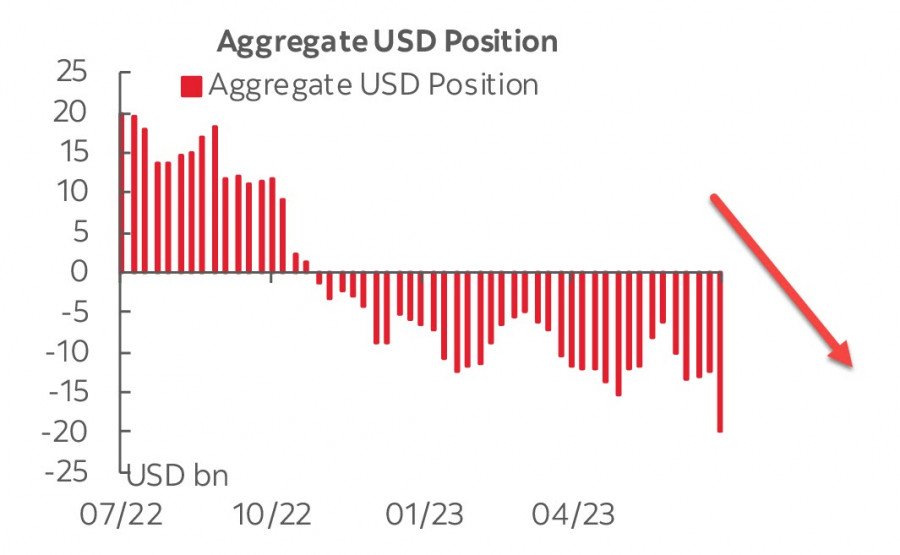

CFTC data reflects a significant deterioration in sentiment towards the US dollar. The overall short position on the USD increased by 7.39 billion during the reporting week, reaching -19.88 billion, marking the largest weekly change since 2020, and the highest bearish bias since 2021.

Significant corrections were observed in positions on the euro and yen. In addition, it is worth noting that the net long position on gold increased by a substantial 6.231 billion, reaching 38.258 billion. Buying gold while simultaneously selling the dollar often signifies expectations that the dollar will weaken.

The Federal Reserve's rate hike on Wednesday is considered a done deal, and the market's primary focus will be on the forecasts. The Fed's main goal is to lower inflation expectations and reduce demand until this objective is achieved. Retail sales data for June indicates high consumer activity, suggesting a potential threat to sustainable core inflation.

The prospects for the dollar remain unclear. Either tightening financial conditions will lead to a sharp decline in consumption, creating conditions for a recession, or the transition will be more gradual. In the first case, the dollar will weaken, while in the second, any corrective decline may be short-lived, as the eurozone economy is closer to a recession than the US economy.

EUR/USD:

On Thursday, the ECB meeting will take place, and a 25 bps rate hike is considered a done deal, as Council members have repeatedly communicated in their comments. The rate hike itself is unlikely to cause a significant movement.

The main focus will be on the forecasts, from which the market will obtain information about the plans for the September meeting - either another rate hike will be announced, or the European Central Bank will take a pause. These post-meeting data will be the factor that either pushes the euro higher or allows for a strengthening of the corrective decline.

The eurozone economy is slowing down, and the PMI data published on Monday came out worse than expected in all sectors - both in manufacturing and services. The slowdown in activity suggests that inflation deceleration will continue, and the September meeting will be the last one where the ECB raises rates. If the market confirms this assumption, the euro will turn down, and the bullish trend will come to an end.

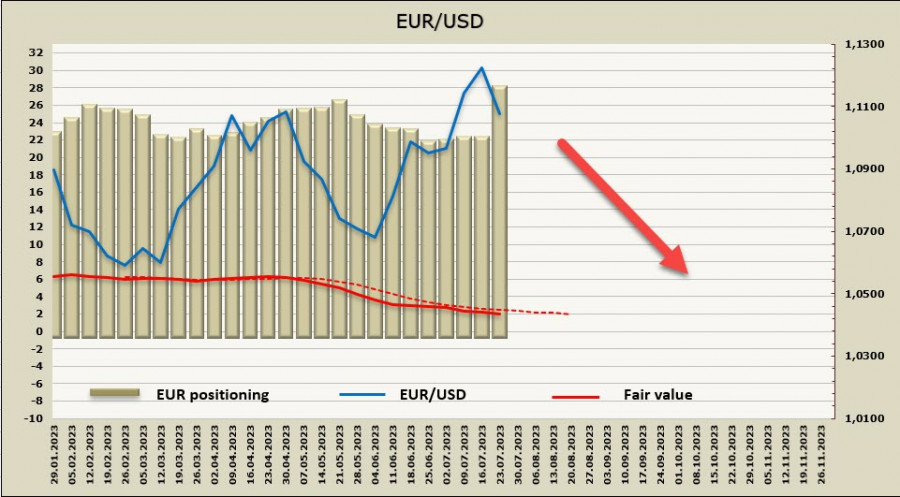

The net long position on the euro increased by 5.8 billion during the reporting week, marking the most significant improvement in sentiment towards the euro since September of last year. The calculated price has not yet turned upwards.

Investors seem to be anticipating the end of the Fed's rate hike cycle and the completion of the bullish impulse in the US dollar. On Wednesday, the FOMC meeting will take place, and the expected rate hike is already fully priced in. As a result, the yield spread will start to favor the euro, as the ECB is still far from the end of its rate cycle. It is assumed that the FOMC's completion of the rate cycle will be accompanied by hawkish comments, which could lead to further decline in EUR/USD towards the support level at 1.1010/20. Considering the significant change in sentiment on futures after the formation of a local base, the euro will likely attempt to resume its growth.

GBP/USD:

The retail sales data published on Friday for June came out better than expected, supporting the pound as the maintenance of high consumer demand also implies the preservation of high inflation expectations and, consequently, an increase in the Bank of England's rate forecasts.

At the same time, business activity is slowing down faster than expected - the PMI in the manufacturing sector declined from 46.5 to 45 in July, while in the services sector, it decreased from 53.7 to 51.5. The composite index also slowed down from 52.8 to 50.7. Considering that GDP growth is minimal and the UK economy is half a step away from a recession, maintaining high consumption while PMI activity declines implies a transition to a stagflation regime, which combines high inflation and recession. This is the most nightmarish scenario for the Bank of England, which they would like to avoid.

Inflation in the UK is higher than in the eurozone and the US, which suggests further rate hikes by the BoE even before the threat of a recession. This factor will support demand for the pound in the short term.

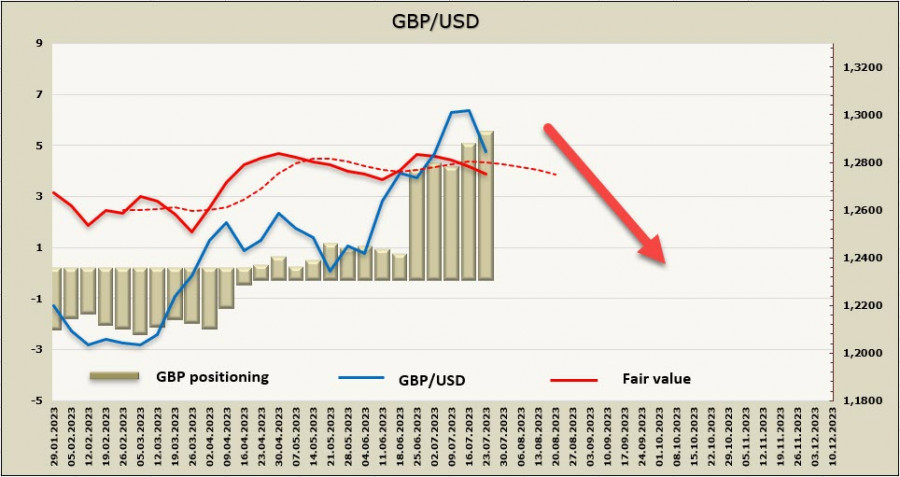

The net long position on GBP increased by 499 million during the reporting week, reaching 5.192 billion, reflecting bullish positioning. The calculated price is currently pointing downwards, which suggests an attempt to develop a corrective decline.

The pound has fallen below the support level at 1.2847, which technically indicates the possibility of a downward movement. The next support is at 1.2770/90, where the lower boundary of the long-term bullish channel lies. Considering that speculative positioning in futures is shifting in favor of the pound, we assume that the downward attempts are of a corrective nature, and the pound is unlikely to fall below 1.2770. After forming a local peak, the upward trend is expected to resume.

The material has been provided by InstaForex Company - www.instaforex.comfrom Forex analysis review https://ift.tt/V4TdNBt

via IFTTT